Share this

by Valentin Kalinov on Jan 3, 2023 2:11:00 PM

This article was written right after the FTX collapse, and it perfectly fits the discussion around crypto investments in times when crypto is in a bear market and experiences high volatility. There is never the perfect time when it comes to investing in crypto. Trying to time the market is challenging, especially for inexperienced investors. One often neglected strategy is Dollar Cost Averaging (DCA). Dollar-cost averaging is investing a fixed amount of money regularly, regardless of the crypto price. Dollar-cost averaging may also help prevent your emotions from undermining your portfolio performance. Many crypto exchanges and financial institutions offer users DCA strategies. However, almost all of the market solutions are custodial, meaning that users do not have control over their private keys. Many users prefer to keep their portfolios on exchanges because of the ease of use. The exchange handles key management, trading, and fiat on-ramps in one place. User-controlled wallets, on the other hand, offer personal control over one’s tokens. Private keys are in the sole custody and responsibility of the user. Trading becomes more challenging as it requires deeper knowledge and different type of risk management. Mean Finance offers non-custodial DCA for users while not relying on centralized exchanges. Users can pick the assets they want to invest and the frequency of investment and let the strategy work for them.

Authors: Valentin Kalinov, Christian Viehof

At least 75 crypto exchanges have closed down due to hacks, scams, or disappeared for unknown reasons in 2020. The collapse of FTX again raises the question of self-custody vs. custodial wallets. Of course, financial institutions are only limited to working with centralized companies like FTX, but the average user trading crypto is not limited to centralized solutions. Often DCA makes more sense as a strategy for people instead of actively trading and trying to time the market. Here are a few reasons why people should consider DCA:

- People who want to get the best average price on an asset over a long period of time.

- People who aren’t professional traders.

- People who succumb to emotions such as the fear of missing out.

Research shows that buying a little bit each day, or every week, will result in higher returns compared to trading as a non-professional.

Mean Finance and DCA

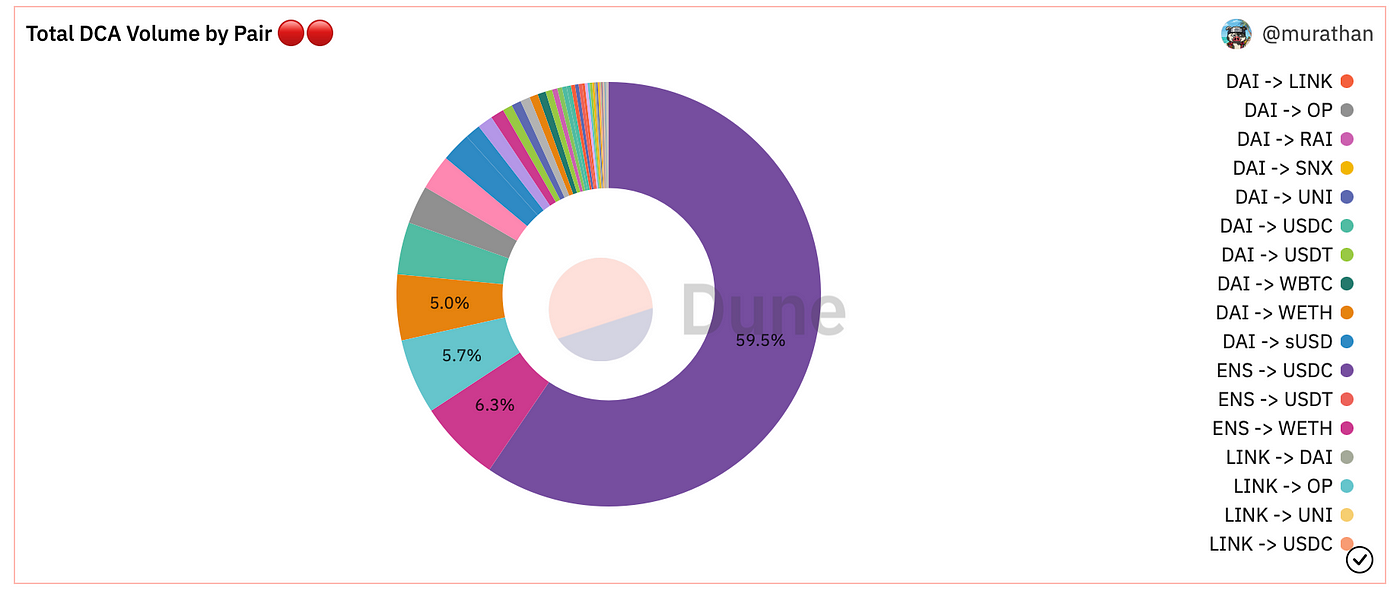

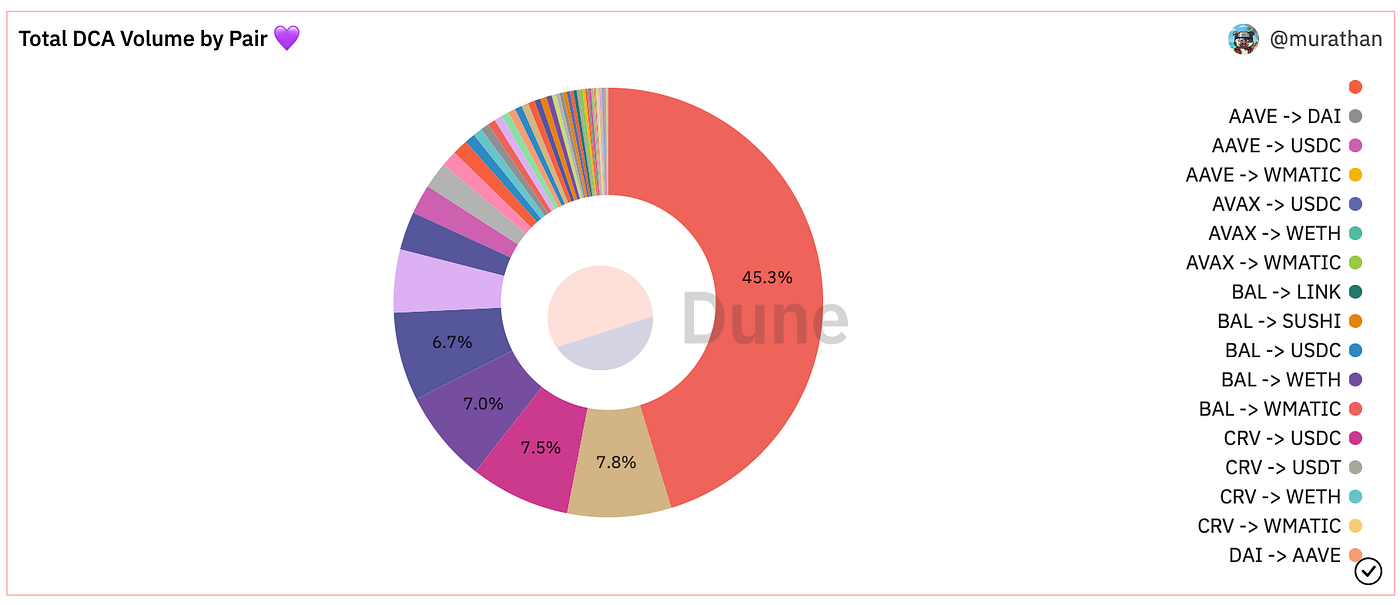

Mean Finance is an open protocol that enables users (or dApps) to dollar cost average ERC20 into any ERC20 with their preferred period frequency without sacrificing decentralization or giving up personal information to any centralized parties. The protocol enables users to set up actions like swapping between pairs of tokens. For example, one could set up an ERC-20 pair DCA order where a stablecoin is exchanged daily for another asset. Even though such an operation would seem simple and could be executed manually, there is the problem of gas fees for each purchase. Mean Finance elegantly solves the gas challenge. Users don’t have to pay for their swaps to be executed after setup. The users only pay fees when interacting with their positions (for example, by adjusting the buy intervals). The protocol introduces participants called swappers (AKA market makers) whose role is to execute individual transactions. Incentives for swappers include arbitrage opportunities between the oracle aggregator and external DEXes, rewards for providing liquidity to balance out swaps, and a sharing of the 0.6% protocol fees applicable to each position. When users interact with their positions, no protocol fee is charged. Protocol fees are collected only on swaps. As of now, that fee is 0.6%.

Each position in Mean Finance is represented as an NFT. The dynamic NFT not only represents the ownership of the strategy but also displays information (like the pairs, amount invested, and frequency) about the position. Additionally, the NFT allows users to grant access rights to their position. For example, an additional address can be granted access to increase the invested sum or withdraw funds from the swapped balance. Transferring the NFT transfers the ownership of the DCA strategy as well.

A recent feature introduced by Mean Finance is yield generation during DCA. When users set up their investment, they can specify a yield-bearing assets to generate yield while the position gets executed. For example, if one sets up a USDC -> ETH position, they can earn a yield on both USDC and ETH. Yield generation works only with supported assets. The first integration for yield generation was with Aave.

Since Mean Finance is a decentralized protocol, other dApps can integrate with it and offer the functionality to their users. These could be other DeFi protocols or maybe wallet providers. What if a DAO treasury engages in DCA on WBTC? All possible uses-cases have not yet been explored.

As of today Mean Finance supports Polygon, Arbitrum One and Optimism.

The International Token Standardization Association (ITSA) e.V.

The International Token Standardization Association (ITSA) e.V. is a not-for-profit association of German law that aims at promoting the development and implementation of comprehensive market standards for the identification, classification, and analysis of DLT- and blockchain-based cryptographic tokens. As an independent industry membership body, ITSA unites over 100 international associated founding members from various interest groups. In order to increase transparency and safety on global token markets, ITSA currently develops and implements the International Token Identification Number (ITIN) as a market standard for the identification of cryptographic tokens, the International Token Classification (ITC) as a standard framework for the classification of cryptographic tokens according to their inherent characteristics. ITSA then adds the identified and classified token to the world’s largest register for tokens in our Tokenbase.

- The International Token Identification Number (ITIN) is a 9-digit alphanumeric technical identifier for both fungible and non-fungible DLT-based tokens. Thanks to its underlying Uniform Token Locator (UTL), ITIN presents a unique and fork-resilient identification of tokens. The ITIN also allows for the connecting and matching of other media and data to the token, such as legal contracts or price data, and increases safety and operational transparency when handling these tokens.

- The International Token Classification (ITC) is a multi-dimensional, expandable framework for the classification of tokens. Current dimensions include technological, economic, legal, and regulatory dimensions with multiple sub-dimensions. By mid-2021, there will be at least two new dimensions added, including a tax dimension. So far, our classification framework has been applied to 99% of the token market according to the market capitalization of classified tokens.

- ITSA’s Tokenbase currently holds data on over 4000 tokens. Tokenbase is a holistic database for the analysis of tokens and combines our identification and classification data with market and blockchain data from external providers. Third-party data of several partners is already integrated, and API access is also in development.

Remarks

If you like this article, we would be happy if you forward it to your colleagues or share it on social networks. More information about the International Token Standardization Association can be found on the Internet, on Twitter, or on LinkedIn.

Valentin Kalinov is an Executive Director at International Token Standardization Association (ITSA) e.V., working to create the world’s largest token database, including a classification framework and unique token identifiers and locators. He has over five years of experience working at BlockchainHub Berlin in content creation and token analysis, as a project manager at the Research Institute for Cryptoeconomics at the Vienna University of Economics and token analyst at Token Kitchen. You can contact Valentin via valentin.kalinov@itsa.global and connect on Linkedin if you would like to further discuss ITSA e.V. or have any other open questions.

Christian Viehof is an Executive Director at the International Token Standardization Association (ITSA) e.V., working to create the world’s largest token database including a classification framework and unique token identifiers and locators. He completed his Bachelor in Economics at the University of Bonn, the Hong Kong University and the London School of Economics and Political Science with a focus on Behavioral Economics and Finance. Currently pursuing his Master of Finance at the Frankfurt School of Finance and Management, you can contact him via christian.viehof@itsa.global and connect with him on Linkedin, if you would like to further discuss ITSA e.V. or have any open questions.