Share this

by Valentin Kalinov on Sep 5, 2022 1:08:00 PM

Miner Extractable Value (MEV) is a market manipulation mechanism in a blockchain network by adding, removing, or changing the order of transactions in a block. As the name suggests, miners can reorder transactions in a block resulting in a lost value for traders. Since 2020, the total MEV has amounted to an estimated USD 550–650 million on just the Ethereum network. The problem persists not only on Ethereum but also on other blockchain networks. In traditional markets, when parties wish to exchange value, they go to a clearing house like the New York Stock Exchange that promises to execute their trades in order and fairly. However, there is no such guarantee by the miners when creating a block. As a result, reorganizing the transactions in a block could lead to an unfair advantage for a malicious party. The miner or a third party may perform these attacks directly via the Ethereum gas price auction. In traditional finance, this practice would resemble front-running and is deemed illegal.

Authors: Valentin Kalinov, Christian Viehof

How MEV works?

First, we need to understand how blockchains work. In the context of DeFi, users often look for arbitrage opportunities. If a user spots a such opportunity, they create and submit their transaction to the mempool. The mempool is the place where all unconfirmed transactions get collected. Miners pick the transactions with the highest gas price and order them by gas spent in the block they produce. Transactions are then executed by their order. If two equal transactions end up in the block, the one paying higher fees gets executed, and the second one fails. Miners indirectly profit from the traders’ transaction fees since even failed transactions pay for gas, leading to higher fee revenues for miners.

There are different types of MEV attacks. The miners or a third party can execute these. In each case, the attack is executed by an automated bot:

- Front-running: the ability of miners or bots to insert transactions before a victim transaction for profit.

- Back-running: placing a transaction in a block directly after a user transaction.

- Sandwich trading: Execute trades both before and after a user. Sandwich attacks commonly occur on DEXs (Decentralized Exchanges), where they involve the front-running of an order to manipulate the price against it, followed by a back run enabling the attacker to profit at the victim’s expense.

- Censorship attacks: An adversary may spam the blockchain with transactions to prevent users and bots from issuing transactions. An example attack would be preventing a user from liquidating a debt position where the collateral drops below the safe levels. By spamming transactions, an adversary might force-liquidate the targeted user.

- Non-Fungible Tokken (NFT) MEV: Following the growth of the NFT ecosystem, we can observe NFT-specific attacks. Bots can be programmed to be the first in line to buy new NFT collections.

Researchers believe miners are still leaving money on the table by not acting on the mentioned opportunities. If reordering transactions leads to higher revenues for miners, it is expected that reordering of transactions will only grow in the future. The issue could even escalate to a level where miners reorg blocks mined by other miners in an attempt to steal the MEV. Such actions might lead to chain instability.

Solutions

A number of organizations, companies, and researchers are working on solutions for MEV extraction. In general, there are two camps. Some believe that MEV should not be tolerated and banned; others believe that MEV will exist in the future and the way forward will be to democratize MEV to prevent centralization.

Chainlink

The proposed Fair Sequencing Service (FSS) by Chainling is a mechanism that enables Decentralized Finance (DeFi) systems to reduce transaction sequencing issues and costs. The idea behind FSS is to have an oracle network order the transactions sent to a particular contract.

Flashbots

Flashbots is a research and development organization focused on the impact MEV.

Flashbots is an independent project which extends the go-ethereum client with a service that allows searchers to submit MEV transactions to miners without revealing them to the public mempool. This prevents transactions from being frontrun by generalized frontrunners.

MEV Boost

MEV-Boost is an implementation of proposer-builder separation (PBS) built by Flashbots for Ethereum’s Proof-of-Stake (PoS) algorithm. MEV-Boost allows validators to maximize their staking rewards by selling blockspace on an open market place. Like Flashbots this solution tries to democratize MEV extraction.

Arbitrum

Arbitrum is an Ethereum optimistic rollup that has committed to a zero MEV extraction. Arbitrum offers a First Come First Serve (FCFS) ordering of transactions which are collected by a so-called Sequencer. The Arbitrum flagship chain will eventually have a distributed set of independent parties controlling the Sequencer.

Shutter Network

Shutter allows users to send encrypted transactions in a way that protects them from front runners.

Shutter Network is an open-source project that aims to prevent front running on Ethereum by using a threshold cryptography-based distributed key generation (DKG) protocol.

Researchers hope that MEV Boost and, in the future, Proposer-Builder Separation via danksharding will help to mitigate MEV’s real threats to a permissionless and decentralized Ethereum and will continue to further help reduce gas fees and network congestion for users. For now, it is recommended to use L2s like Arbitrum and DEX aggregators (these significantly reduce the MEV risk) when trading on-chain.

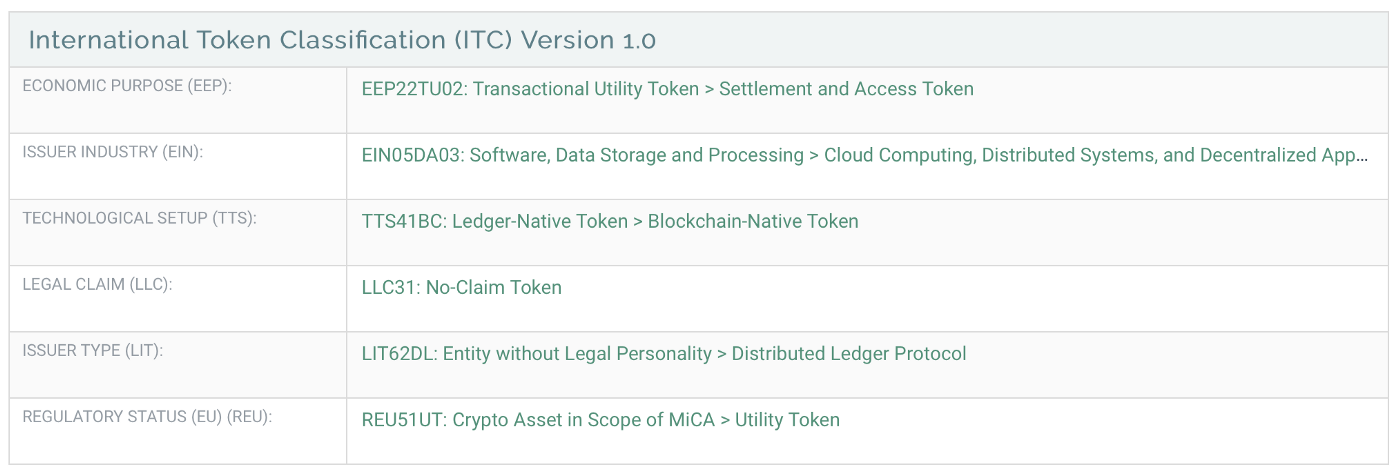

The classification of Ethereum (ETH) according to the ITC:

Economic Purpose (EEP): ETH is listed as a settlement and access token (EEP22TU02).

Industry Type (EIN): The issuer of ETH is active in the field of CloudComputing, Distributed Systems and Decentralized Applications (EIN05DA03).

Technological Setup (TTS): ETH is a Blockchain-Native Token (TTS41BC).

Legal Clam (LLC): The ETH token does not entitle its holder to any legal claim or rights against the issuing organization therefore it is listed as a No-Claim Token (LLC31).

Issuer Type (LIT): The dimension “Issuer Type” provides information on the nature of the issuer of the token. Ethereum is an Entity without Legal Presonality and it is Distributed Ledger Protocol (LIT62DL)

Regulatory Framework (EU) (REU): The dimension “Regulatory Status EU” provides information on the potential classification of a token according to the European Commission’s proposal for a Regulation on Markets in Crypto Assets (MiCA, Regulation Proposal COM/2020/593 final). The ETH token qualifies as a Utility Token; Crypto Asset in the Scope of MiCA (REU51UT) according to the definition provided in Article 3 (5) of Regulation Proposal COM/2020/593 final.

References

- Maximal extractable value (MEV), ethereum.org

- Miners as intermediaries: extractable value and market manipulation in crypto and DeFi, bis.org

- Zeromev, info.zeromev.org

- Example sandwich attack, twitter.com

- Flashbots Docs, docs.flashbots.net

- Ethereum is a Dark Forest, paradigm.xyz

- Quantifying MEV: Introducing MEV-Explore v0, medium.com

- Quantifying Blockchain Extractable Value: How dark is the forest?, arxiv.org

- Flashbots — Frontrunning the MEV Crisis, writings.flashbots.net

- What is MEV Boost?, alchemy.com

- MEV Boost in a Nutshell, boost.flashbots.net

The International Token Standardization Association (ITSA) e.V.

The International Token Standardization Association (ITSA) e.V. is a not-for-profit association of German law that aims at promoting the development and implementation of comprehensive market standards for the identification, classification, and analysis of DLT- and blockchain-based cryptographic tokens. As an independent industry membership body, ITSA unites over 100 international associated founding members from various interest groups. In order to increase transparency and safety on global token markets, ITSA currently develops and implements the International Token Identification Number (ITIN) as a market standard for the identification of cryptographic tokens, the International Token Classification (ITC) as a standard framework for the classification of cryptographic tokens according to their inherent characteristics. ITSA then adds the identified and classified token to the world’s largest register for tokens in our Tokenbase.

- The International Token Identification Number (ITIN) is a 9-digit alphanumeric technical identifier for both fungible and non-fungible DLT-based tokens. Thanks to its underlying Uniform Token Locator (UTL), ITIN presents a unique and fork-resilient identification of tokens. The ITIN also allows for the connecting and matching of other media and data to the token, such as legal contracts or price data, and increases safety and operational transparency when handling these tokens.

- The International Token Classification (ITC) is a multi-dimensional, expandable framework for the classification of tokens. Current dimensions include technological, economic, legal, and regulatory dimensions with multiple sub-dimensions. By mid-2021, there will be at least two new dimensions added, including a tax dimension. So far, our classification framework has been applied to 99% of the token market according to the market capitalization of classified tokens.

- ITSA’s Tokenbase currently holds data on over 4000 tokens. Tokenbase is a holistic database for the analysis of tokens and combines our identification and classification data with market and blockchain data from external providers. Third-party data of several partners is already integrated, and API access is also in development.

Remarks

If you like this article, we would be happy if you forward it to your colleagues or share it on social networks. More information about the International Token Standardization Association can be found on the Internet, on Twitter, or on LinkedIn.

Valentin Kalinov is an Executive Director at International Token Standardization Association (ITSA) e.V., working to create the world’s largest token database, including a classification framework and unique token identifiers and locators. He has over five years of experience working at BlockchainHub Berlin in content creation and token analysis, as a project manager at the Research Institute for Cryptoeconomics at the Vienna University of Economics and token analyst at Token Kitchen. You can contact Valentin via valentin.kalinov@itsa.global and connect on Linkedin if you would like to further discuss ITSA e.V. or have any other open questions.

Christian Viehof is an Executive Director at the International Token Standardization Association (ITSA) e.V., working to create the world’s largest token database including a classification framework and unique token identifiers and locators. He completed his Bachelor in Economics at the University of Bonn, the Hong Kong University and the London School of Economics and Political Science with a focus on Behavioral Economics and Finance. Currently pursuing his Master of Finance at the Frankfurt School of Finance and Management, you can contact him via christian.viehof@itsa.global and connect with him on Linkedin, if you would like to further discuss ITSA e.V. or have any open questions.