Share this

by Christian Viehof on Jul 4, 2023 5:59:00 PM

This is a guest article by Rudy Capital. You can find the original article here.

GMX’s initial version distinguished itself by offering a decentralized spot and perpetual exchange that supported low swap fees and zero price impact trades, an attractive proposition for both casual and professional traders.

The backbone of the GMX trading infrastructure was GLP, a unique multi-asset pool, that allowed liquidity providers to earn fees from various sources, including market making, swap fees, and leverage trading.

Despite these impressive attributes, the GMX DAO has identified room for improvement and potential vulnerabilities in their original design. As a result, they have launched an upgraded version — GMX v2. This new iteration aims to increase efficiency, reduce risk, and further enhance the user experience. Notable changes include the shift to isolated markets, integration of Chainlink’s low-latency oracles, a reduction in trading fees, and the introduction of price impacts and funding fees.

We will explore each of these transformative changes in the following sections, shedding light on how they augment the user experience in GMX v2 and fortify GMX’s standing in the shark tank of DeFi derivatives.

What’s new?

- There are now isolated markets, so liquidity providers now have a choice of which assets they want to provide liquidity for.

- Price impact and funding fees have been implemented to balance shorts and longs and prevent the risk of price manipulation.

- To increase efficiency and mitigate front-running, Chainlink’s low latency oracles have been integrated.

- Stop Loss and Take Profit orders no longer require an open position to be set and thanks to Chainlink’s low-latency oracles, execution at the set price is much more likely.

- The spot and perpetual fees were halved from 0.1% to 0.05%.

The Advent of Isolated markets

The shift from multi-asset trading through the GLP pool to isolated markets forms the backbone of GMX v2. This change signals a departure from the GLP model where multiple tokens such as Bitcoin, Ethereum, Uniswap, Chainlink, USD Coin, Tether, Dai, and Frax, could be traded through the same pool. Now, each isolated market supports trading between distinct pairs of assets.

For instance, an ETH-USD market has been created, offering both spot and perpetual trading options. In this market, each pair is constructed using a long collateral token, a short collateral token, and an index token. ETH serves as the long collateral token, a stablecoin is the short collateral token, and the index token is also ETH. Similar isolated market structures extend to other pairs like BTC/USD and SOL/USD, each using WBTC and ETH respectively as long collateral tokens.

Liquidity providers now have the option to deposit either the long or short collateral token, or both, in order to mint GM liquidity provider tokens. This change presents a risk management advantage by isolating market risks; liquidity providers bear risk only within the specific market where their deposit is made. Consequently, this setup enables the possibility of permissionless listings.

Notably, synthetic markets have been introduced, creating markets when the index tokens aren’t among the principal assets of Ether, USD Coin, Bitcoin, Tether, and Dai. As demonstrated in Figure 1, this advancement brings GMX v2’s operation closer to Synthetix, though the implementation differs, given that Synthetix’s Synths rely solely on $SNX as collateral, while GMX v2 employs highly liquid assets.

In essence, the transformation to isolated markets is a pivotal evolution in GMX v2. It not only bolsters risk management and offers liquidity providers more control, but it also lays the groundwork for more sophisticated features and innovation on the GMX platform.

Incorporation of Price Impact and Funding Fees

One of GMX v1’s key attractions was the capability to execute large, slippage-free trades, a feature that greatly appealed to professional and high-net-worth traders. However, this unique selling proposition also faced criticism, as some, like the founder of ZigZag, argued it could potentially encourage price manipulation.

GMX v2 addresses these concerns by introducing price impact and funding fees, changes that have been met with mixed reactions. While these features may appear unfavorable to traders accustomed to trading without price slippage, they represent a considerable enhancement for liquidity providers by mitigating the risk of price manipulation.

In GMX v1, only borrowing fees alongside a base 0.1% open and close fee existed. However, GMX v2 also introduces a funding fee to maintain balance between long and short positions, protecting liquidity providers’ funds. This change is critical as shown in Figure 2; GMX often experienced a large open interest where either short or long positions dominated. In scenarios where traders significantly profited during major price swings, liquidity providers were left to cover the losses. Suppose we envision a scenario similar to the bull market of 2020/2021, where traders heavily invest in long positions with leverage. In such a situation, there is a possibility that GLP will not be able to maintain its targets weights as it is composed of more and more stablecoins and GLP Liquidity Providers will no longer benefit from the price increases of volatile assets such as Ether or Bitcoin, causing them to incur significant losses. However, such a situation could also happen in a bear market, which would be even more critical, since GLP then consists mainly of volatile assets, which, in contrast to stablecoins, lead to additional losses due to their price decline.

This reality is reflected in Figure 3, which shows that since the start of 2023, traders have consistently profited at the expense of GLP Liquidity Providers. These newly introduced funding fees and price impact reduce this risk for liquidity providers by redistributing the risk more equitably. The trade-off here, of course, is that traders must now account for these additional costs, which may affect the protocol’s attractiveness, particularly to large volume traders.

The upshot of these adjustments is that they demonstrate GMX’s commitment to the stability and longevity of the protocol. By recalibrating the distribution of risk, they ensure a more sustainable trading environment that benefits all users in the long term.

Integration of Chainlink Low-Latency Oracles

In a bid to enhance the efficiency and security of the platform, GMX v2 is integrating Chainlink’s low-latency oracles following a successful governance proposal. Unlike Chainlink Price Feeds, which deliver on-chain updates, this new oracle solution adopts a pull-based approach that generates per-block oracle reports. Users can retrieve these reports off-chain and validate them atomically with their on-chain transactions, as illustrated in Figure 4.

The integration of Chainlink’s low-latency oracles into GMX v2 offers several compelling advantages. First, it substantially reduces latency, providing per-block updates that allow users to access faster, more timely information. Second, it effectively mitigates frontrunning risks by maintaining price privacy until transactions are settled, preventing potential arbitrageurs from exploiting pricing information. Lastly, it enhances gas efficiency by streamlining the validation process of oracle updates, thus eliminating the need for data to be published on a separate blockchain before on-chain delivery.

However, this exclusive partnership with Chainlink does come with an additional cost. Specifically, GMX will cede 1.2% of the protocol fees to Chainlink, which currently equates to around $2–3M annually. Importantly, these costs won’t be passed on to liquidity providers; instead, they will be covered by the 10% of protocol fees allocated to the GMX treasury. Despite the costs, the integration of Chainlink’s low-latency oracles provides a distinct feature that sets GMX apart in the DeFi space, underscoring the protocol’s commitment to innovation and security.

New Order Types and Reduced Trading Fees

While in GMX v1 you could execute stop loss and take profit orders only after opening a position, with GMX v2 this is now also possible before. For this purpose, the UI will be adapted in the near future. But this is only one of two improvements, because thanks to the Chainlink low latency oracles, both order types are now executed with a significantly higher probability at the set price. This increases confidence in both order types and gives traders greater flexibility and strategic options in managing their positions.

Market Order: An instruction to buy or sell a token immediately at the current market price, without specifying a specific price. It prioritizes speed of execution over obtaining a specific price for the trade.

Limit Order: An instruction to buy or sell a token at a specific price or better. It sets a maximum price for a buy order or a minimum price for a sell order, ensuring that the trade is executed only at the specified price or more favorable.

Stop-loss Order: A type of order placed to limit potential losses on a position. It is set at a specific price below the current market price for a long position or above the current market price for a short position, triggering a market order to sell or cover the position if the price reaches or goes below the specified level, helping to protect against further losses.

Take Profit Order: A type of order placed to secure profits on a position. It is set at a specific price above the current market price for a long position or below the current market price for a short position, triggering a market order to sell or cover the position when the price reaches or goes beyond the specified level, allowing the investor to lock in their desired profits.

In addition to the new order types, GMX has halved its trading fees (from 0.1% to 0.05%), as illustrated in Figure 5. The decision to reduce fees has sparked a lively debate within the GMX community. While some users voiced concerns about how this reduction might affect GMX’s profitability, others believe the lower fees will attract more users, boosting long-term protocol success. The fee reduction can be viewed as compensation for traders, who face the newly introduced price impact and funding fee, representing a reduction in risk for liquidity providers.

As seen in Figure 6, this proposal has been a subject of extensive discussion in the GMX forum (source: https://shorturl.at/eBY56). If the fee reduction doesn’t increase trading volume as intended, the GMX community has the option to adjust it through a governance vote. Nevertheless, the lower fees present a challenge to other platforms like Synthetix, which typically charge higher rates.

The Path Forward for GMX v2

With GMX v2’s debut, the GMX community faces a substantial shift as many key features change. The new model introduces a price impact and a funding fee, which mark a considerable departure from the GMX v1 framework. High-volume traders like Andrew Kang may face a new trading landscape, and their reactions to these changes will be closely watched. GMX has long enjoyed a reputation as an advantageous market for perpetual futures trading, and this could continue with the innovations and reduced fees offered in v2. Nonetheless, centralized platforms like Binance, offering more liquidity albeit at the cost of decentralization, may regain some appeal.

Interestingly, the changes in GMX v2 are likely to have a limited impact on smaller traders, due to the introduced price impact. As such, these modifications could be seen as a move towards a more democratic, ‘for the people’ trading platform. Furthermore, it’s worth noting that sizable and profitable traders have previously posed a challenge to the protocol, as their gains often translated into losses for GLP liquidity providers.

The partnership between Chainlink and GMX adds a unique element to GMX’s offering. By integrating Chainlink’s low-latency oracles, despite incurring some additional fees, GMX creates a distinct selling proposition that adds value to its users. This collaboration paves the way for a new standard, potentially benefiting many DeFi applications and enhancing user fund security.

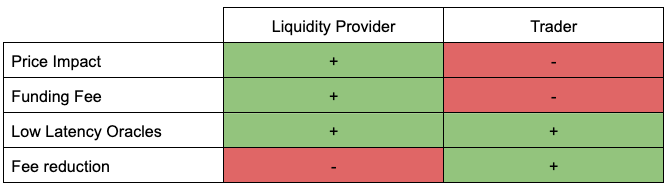

Indeed, the shift in risk distribution between traders and liquidity providers, primarily due to the price impact and funding fee, is a critical aspect of GMX v2. While the reduction in fees from 0.1% to 0.05% is a minor consolation, the trader community’s response to this change remains to be seen. As depicted in Figure 7, these modifications and their impact on liquidity providers and traders are summarized. In the short term, the fee reduction may not significantly spur volume growth, and long-term projections are challenging.

However, GMX v2 paves a promising path forward in terms of competitiveness. Compared to alternatives such as Synthetix, which typically levy higher fees with poorer liquidity, GMX v2 appears to be a compelling choice. These innovations also highlight GMX’s commitment to continuous evolution, striving to optimize their platform.

In the past, a bull market in perpetual future trading without price impact and funding fees could have posed significant risks to liquidity providers. Therefore, the introduction of GMX v2 seems timely, especially as a Bitcoin halving event looms in the not-too-distant future.

Authors

Christian Viehof is Chief Research Officer at Rudy Capital. Feel free to reach out and connect via christian.viehof@rudy.capital and Linkedin.

Thomas Faber is Co-Founder and Chief Investment Officer of Rudy Capital. Feel free to reach out and connect via thomas.faber@rudy.capital and LinkedIn.

About Rudy Capital

Rudy Capital is a German-based advisory firm specializing in market research, risk management and portfolio construction in the field of decentralized finance. More information on our website, on LinkedIn and Twitter.

The International Token Standardization Association (ITSA) e.V.

The International Token Standardization Association (ITSA) e.V. is a not-for-profit association of German law that aims at promoting the development and implementation of comprehensive market standards for the identification, classification, and analysis of DLT- and blockchain-based cryptographic tokens. As an independent industry membership body, ITSA unites over 100 international associated founding members from various interest groups. In order to increase transparency and safety on global token markets, ITSA currently develops and implements the International Token Identification Number (ITIN) as a market standard for the identification of cryptographic tokens, the International Token Classification (ITC) as a standard framework for the classification of cryptographic tokens according to their inherent characteristics. ITSA then adds the identified and classified token to the world’s largest register for tokens in our Tokenbase.