Share this

by Christian Viehof on Jan 9, 2023 2:29:00 PM

Stablecoins have seen increased usage in DeFi. Users now can lend or borrow them on platforms like Aave or provide them as liquidity on DEXs such as Uniswap. Apart from enabling investment opportunities, they provide an easy medium of exchange for traders to go in and out of their positions without returning to fiat. As a result, traders can trade quickly and mitigate the risks of price fluctuations by keeping their profits in fiat-pegged tokens.

Authors: Thomas Faber, Christian Viehof

However, if you take a closer look at fiat-pegged stablecoins, you quickly realize that there isn’t much choice. Tether, USD Coin and Binance USD claim almost 90% of the market share. All three stablecoins have a peg to the US dollar, which begs the question why the euro is almost completely irrelevant in DeFi. There are two main reasons for this:

- Regulatory uncertainties regarding MiCA and the digital euro.

- A negative deposit rate at the ECB (is now positive) made holding cash very expensive.

What type of stablecoins are out there?

We can say that there are three main categories of stablecoins:

- Tokenized funds (e.g., USDC), where a central entity holds cash and cash equivalents such as money market funds and allows the holder to redeem the token for fiat money.

- On-Chain collateralized stablecoins (e.g., DAI), where cryptocurrencies are deposited in a smart contract as collateral and the smart contract issues a stablecoin to the depositor.

- Algorithmic stablecoins (e.g., UST), where the governance token (e.g., LUNA) acts as collateral and the peg is maintained through arbitrage.

The most successful EURO Stablecoins

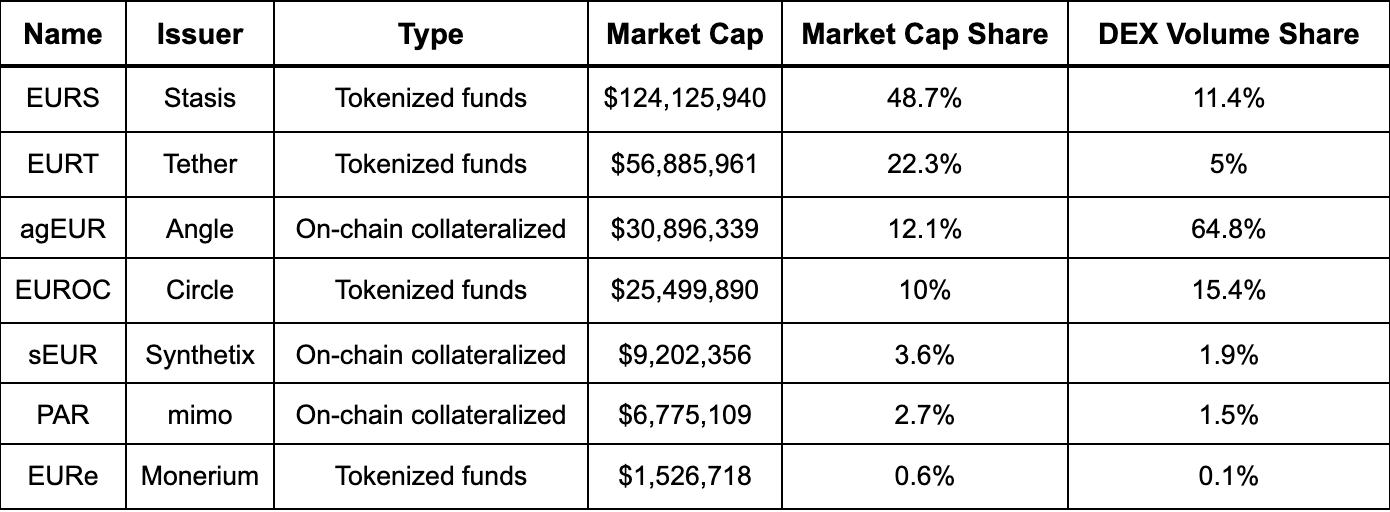

The charts below show the most successful EURO-pegged stablecoins. If you are very interested in metrics, we recommend you check out the Dune Dashboard by Sebventures (MakerDAO Core Team).

What can we take from the data? EURS has the highest market capitalization, but with 11.4% of the volume of DEX trades, it has a very low utilization rate in relation to market capitalization. The same is true for EURT. It is certainly surprising that the censor-resistant agEUR, which is mostly backed by USDC, has by far the highest trading volume in relation to market capitalization. EUROC lands in fourth place in terms of market capitalization but manages to generate more volume than EURS and EURT despite its low market capitalization.

Where are the stablecoins mostly traded?

The two most commonly used DEXs are Uniswap and Curve. Uniswap V3 is known to have high capital efficiency through concentrated liquidity and, thus, low slippage trades. Curve uses a stable automated market maker (stable AMM) to guarantee a close to 1:1 exchange ratio even in unbalanced pools (e.g., 10% USDC, 10% DAI, and 80% USDT).

Whereas with Curve you are primarily compensated with reward tokens (CRV), with Uniswap you receive your underlying (e.g., your return will be in EUROC and USDC, if you provide them as liquidity on Uniswap). In summary, both DEXs have their advantages and disadvantages. Uniswap is more maintenance-intensive since concentrated liquidity requires keeping an eye on the price ranges. In addition, the return is paid out in the two assets that are of interest to us, which is good. Curve usually pays less yield, but the strategy is much simpler, which is why yield aggregators like Yearn build many strategies on top of them.

How liquidity provision makes a good foreign exchange rate hedge

Let’s say you have to pay for things in dollars on a regular basis, or you are concerned about the economic situation in the EU. In both cases, it would be a good idea to keep some of your cash reserves in dollars. Is there perhaps a way to hold both dollars and euros at the same time and earn interest on them?

Yes, there is! Because during our regular research activities, we noticed a very interesting pool some time ago and now that the yield has decreased a bit, we have no qualms about sharing our alpha.

The pool was interesting in our eyes not only because of the return but at the same time, it offered us the opportunity to develop a strategy to reduce dollar exposure. It all sounds very exciting, doesn’t it? After all, Circle’s USDC and EUROC are among the most trusted stablecoins out there. Uniswap is also one of the safest exchanges and if you don’t trust Uniswap’s smart contracts, you can get insurance from Nexus Mutual for less than a 1% fee per year. At the same time, the strategy is on Ethereum, which makes gas fees a nagging issue, but not off-time or other exogenous risks like with FTX on Solana. So what’s the catch?

The strategy must be actively managed! It is, therefore, important to check the EURO/DOLLAR rate regularly to see if the liquidity is still in range. Because if the exchange rate is outside the range, you no longer earn a return.

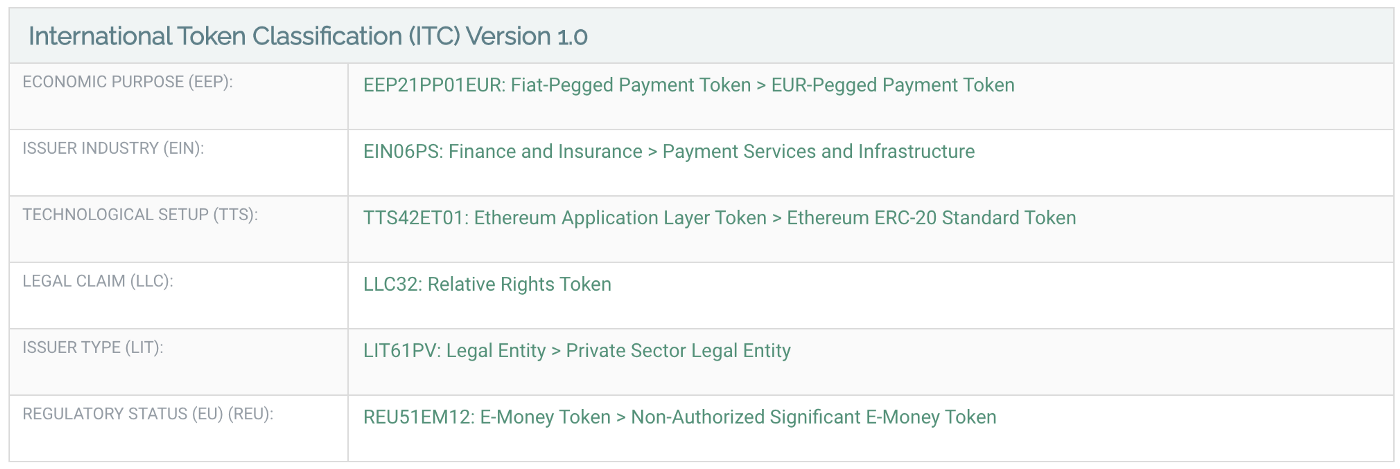

The classification of EUROC according to the ITC:

Economic Purpose (EEP): EUROC is listed as a fiat-pegged payment token (EEP21PP01EUR) similar to the other stablecoins in the industry.

Industry Type (EIN): The issuer of EUROC (Circle) is active in the field of Payment Services and Infrastructure (EIN06PS).

Technological Setup (TTS): EUROC is an Ethereum ERC-20 Standard Token (TTS42ET01). The Class “Ethereum ERC-20 Standard Token” captures every token that is implemented by means of the ERC-20 Standard on top of the Ethereum blockchain.

Legal Clam (LLC): The EUROC token does entitle its holder with a relative right against the issuing organization, therefore it is listed as a Relative Rights Token (LLC32). Each token represents a claim of one Euro against the issuer; Circle.

Issuer Type (LIT): The dimension “Issuer Type” provides information on the nature of the issuer of the token. EUROC is built by Circle Internet Financial Limited, its Issuer Type is a Private Sector Legal Entity (LIT61PV).

Regulatory Framework (EU) (REU): The dimension “Regulatory Status EU” provides information on the potential classification of a token according to the European Commission’s proposal for a Regulation on Markets in Crypto Assets (MiCA, Regulation Proposal COM/2020/593 final). EUROC (Ethereum) qualifies as a Non-Authorized Significant E-Money Token (REU51EM12) according to the definition provided in Article 3 (4) of Regulation (EU) 2019/1937.

References:

- All you need to know about Circle’s Euro-based stablecoin, https://www.cnbctv18.com

- Bitstamp to list the first mainstream euro-pegged stablecoin — EURt, https://blog.bitstamp.net

- Circle announces plans to become a national digital currency bank, https://www.fintechfutures.com

- Firm behind popular US dollar stablecoin to launch Euro Coin., https://www.washingtonpost.com

- Circle’s New Euro-backed Stablecoin Mimics USDC, https://blockworks.co/

- Circle Launches Euro-Backed Stablecoin, https://decrypt.co/

- Circle’s New Euro Stablecoin: Issued from the US and Used Outside the EU?, https://philippsandner.medium.com

- USDC issuer Circle to launch Euro stablecoin this month, https://www.ledgerinsights.com

The International Token Standardization Association (ITSA) e.V.

The International Token Standardization Association (ITSA) e.V. is a not-for-profit association of German law that aims at promoting the development and implementation of comprehensive market standards for the identification, classification, and analysis of DLT- and blockchain-based cryptographic tokens. As an independent industry membership body, ITSA unites over 100 international associated founding members from various interest groups. In order to increase transparency and safety on global token markets, ITSA currently develops and implements the International Token Identification Number (ITIN) as a market standard for the identification of cryptographic tokens, the International Token Classification (ITC) as a standard framework for the classification of cryptographic tokens according to their inherent characteristics. ITSA then adds the identified and classified token to the world’s largest register for tokens in our Tokenbase.

- The International Token Identification Number (ITIN) is a 9-digit alphanumeric technical identifier for both fungible and non-fungible DLT-based tokens. Thanks to its underlying Uniform Token Locator (UTL), ITIN presents a unique and fork-resilient identification of tokens. The ITIN also allows for the connecting and matching of other media and data to the token, such as legal contracts or price data, and increases safety and operational transparency when handling these tokens.

- The International Token Classification (ITC) is a multi-dimensional, expandable framework for the classification of tokens. Current dimensions include technological, economic, legal, and regulatory dimensions with multiple sub-dimensions. By mid-2021, there will be at least two new dimensions added, including a tax dimension. So far, our classification framework has been applied to 99% of the token market according to the market capitalization of classified tokens.

- ITSA’s Tokenbase currently holds data on over 4000 tokens. Tokenbase is a holistic database for the analysis of tokens and combines our identification and classification data with market and blockchain data from external providers. Third-party data of several partners is already integrated, and API access is also in development.

Remarks

If you like this article, we would be happy if you forward it to your colleagues or share it on social networks. More information about the International Token Standardization Association can be found on the Internet, on Twitter, or on LinkedIn.

Authors

Christian Viehof is an Executive Director at the International Token Standardization Association (ITSA) e.V., working to create the world’s largest token database including a classification framework and unique token identifiers and locators. He completed his Bachelor in Economics at the University of Bonn, the Hong Kong University and the London School of Economics and Political Science with a focus on Behavioral Economics and Finance. Currently pursuing his Master of Finance at the Frankfurt School of Finance and Management, you can contact him via christian.viehof@itsa.global and connect with him on Linkedin, if you would like to further discuss ITSA e.V. or have any open questions.

Thomas Faber is the Co-Founder and Chief Investment Officer of Rudy Capital. Feel free to reach out and connect via thomas.faber@rudy.capital and LinkedIn.