Share this

by Valentin Kalinov on Aug 9, 2023 5:41:46 PM

The need for a stable value of transfer in the DeFi space has always been a desired feature. With the recent failure of many algorithmic stablecoins, the conversation on what makes a good stablecoin continues. Centralized counterparts such as Tether (USDT) and USD Coin (USDC) have traditionally dominated the scene, albeit not without their own set of vulnerabilities. However, even USDT and USDC have their weakneses as we withnessed the recent USDC depeg after the collapse of Silicon Valley Bank. In response to this uncertainty, protocols like Aave and Curve have delved into the creation of their own stablecoins. The recent launch of Aave’s GHO coin and Curve’s crvUSD is less a rumor and more a strategic shift. At its core, the development of proprietary stablecoins serves a dual purpose: it enables these protocols to remain autonomous and directly steer the growth trajectory of the stablecoin, while concurrently reducing their dependence on external parties. Additionally, the complete ownership of a stablecoin allows the protocols to consolidate revenue streams within their ecosystems. This further enhances their resilience, independence, and profitability. This dynamic battle between Aave’s GHO and Curve’s crvUSD is not just a contest of supremacy, but a testament to the evolving landscape of stablecoins in the world of decentralized finance.

Authors: Valentin Kalinov, Christian Viehof

An Evolutionary Leap, Not Merely a Revolution

At first glance, both stablecoins exhibit noticeable parallels to the design framework of Dai, the stablecoin devised by Maker. Much like Dai, both Aave’s GHO coin and Curve’s crvUSD employ an overcollateralization strategy and share similar issuance methodologies. Yet, it would be a simplification to label these as mere Dai replicas. Each coin incorporates unique design elements that mirror the ethos and structure of their parent protocols. These distinct characteristics are more than ornamental; they align with the underlying protocol design, providing a testament to the evolution in stablecoin development. The likeness to Dai is less a revolution overthrowing established norms and more an evolution that enhances and refines existing methodologies within the stablecoin space.

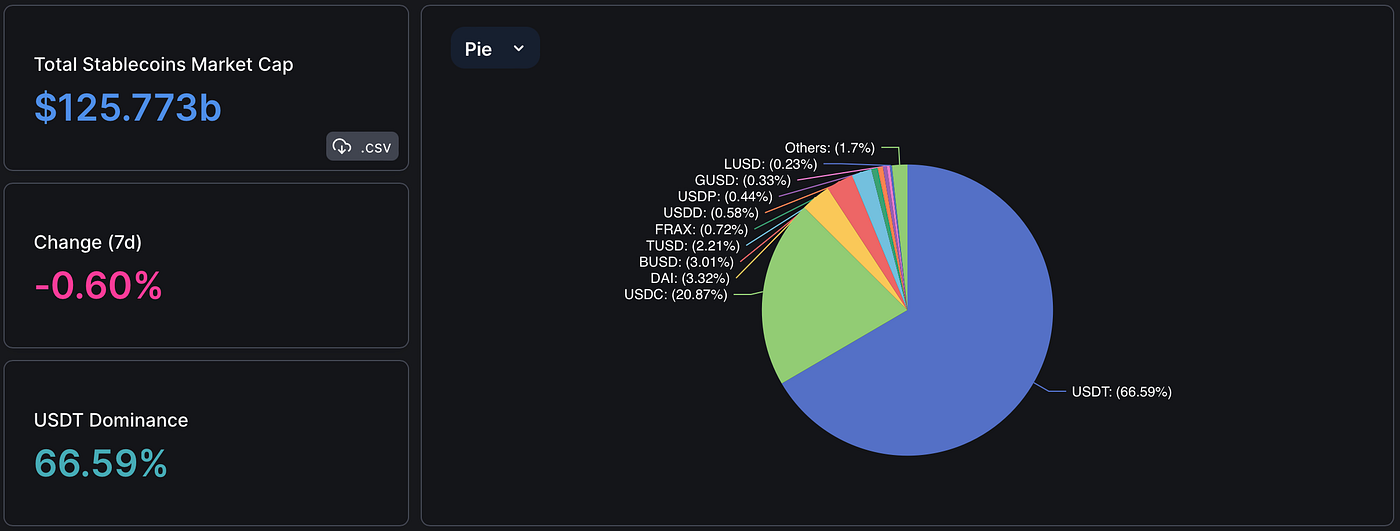

Despite the substantial buzz surrounding these stablecoins, generated by both the crypto-centric media and the broader community, it’s crucial to maintain perspective. Currently, their market share remains considerably dwarfed when compared to dominant players such as Tether and USD Coin.

Even Dai, a stablecoin sharing a similar design philosophy with GHO and crvUSD, only commands a modest market share of less than 4%. The realm of stablecoins remains largely under the sway of Tether, boasting a commanding 66% dominance, followed by USDC, holding a significant 20% share. In comparison, the market shares of both GHO and crvUSD currently seem insignificant.

Nevertheless, it’s essential to remember that both of these coins were introduced in 2023, and are still in the process of demonstrating their competitiveness. Moreover, the overarching strategy of Aave and Curve isn’t solely about market share. The primary intent of these protocols is to use GHO and crvUSD as complementary tools to strengthen their ecosystems and generate increased revenue within their respective DAO frameworks.

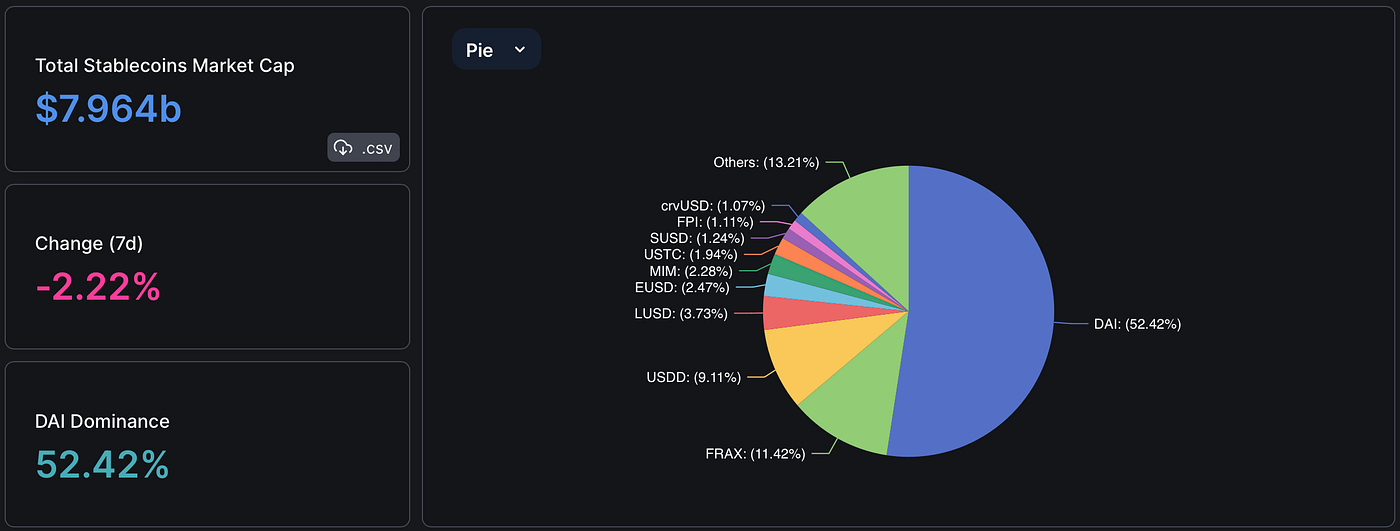

Figure 2 narrows the lens to concentrate on overcollateralized stablecoins that share a design framework akin to DAI. The landscape here paints a familiar picture. Curve’s crvUSD carves out a modest 1% niche, while DAI maintains its dominance with over 50% of the market share. As for Aave’s GHO, having just been launched in July, it is premature to evaluate its market performance or gauge the success of its launch. Only time will reveal its position in this competitive stablecoin market.

Curve’s design decisions

The crvUSD token was launched in early May 2023.

As already mentioned Curve controls the supply of crvUSD with a mint-and-burn mechanism similar to MakerDAO’s DAI.

The LLAMA Algorithm

What sets crvUSD apart from its competitors is its lending-liquidation algorithm known as LLAMA. This innovation continuously rebalances the user collateral in response to crypto price fluctuations, as outlined in the project’s whitepaper.

To simplify, traditional Collateralized Debt Positions (CDPs) operate with a defined liquidation price, a level at which the collateral is liquidated if its value dips below this threshold. In stark contrast, the LLAMA algorithm is a dynamic system that continually adjusts your collateral. In practical terms, if the price of your collateral takes a downturn, the algorithm automatically swaps a portion of your collateral for the borrowed asset, ensuring a balanced position even in volatile market conditions. This represents a fundamental shift in how collateral management is approached within the world of stablecoins.

Adding to its unique appeal, crvUSD’s LLAMA design boasts superior capital efficiency compared to other stablecoins and lending protocols. Rather than locking collateral in a static position, the crvUSD mechanism allows the collateral to be used within CurveFi’s liquidity pools, generating additional yield. This effectively transforms idle capital into productive assets, further enhancing its value proposition within the ever-evolving stablecoin landscape.

Aave’s design descisions

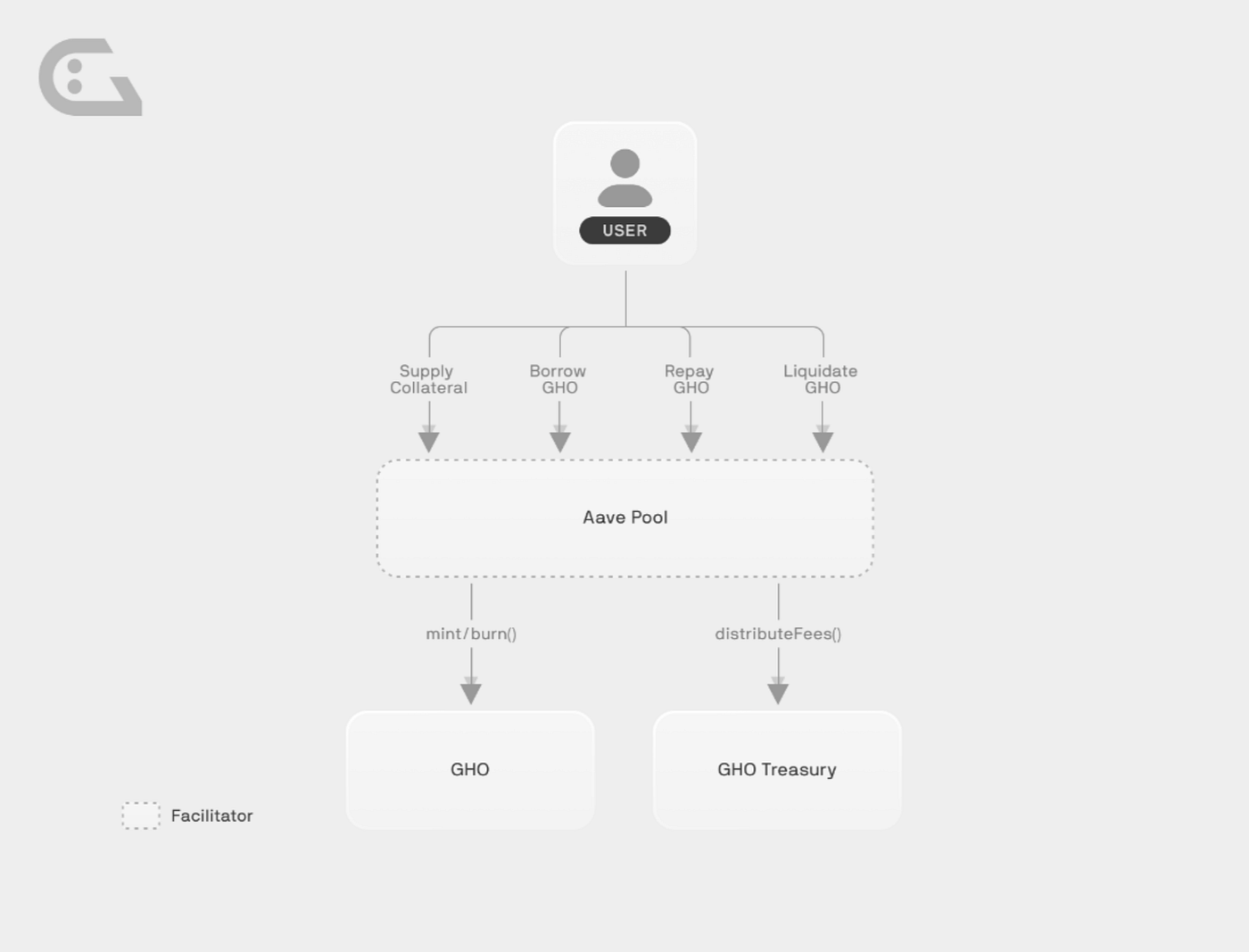

On July 15, Aave DAO has authorized and implemented the proposal for activating GHO, the native, decentralized, over-collateralized asset of the Aave Protocol.

In contrast to other assets borrowed from Aave, where interest earnings are distributed to asset lenders, interest paid on GHO loans are directly funneled into the Aave DAO Treasury. This establishes a unique revenue stream for the DAO, contributing to its self-sustaining ecosystem. Of course, GHO would need to increase its market share in order to make a difference for the DAO Treasury.

GHO is minted under user direction via a variety of strategies. These strategies are enacted by different entities, referred to as “Facilitators,” each with their distinctive approach to GHO integration. Facilitators have the trustless authority to generate (and burn) GHO tokens within the limits of an assigned Bucket. The Bucket’s capacity represents the maximum amount of GHO a particular Facilitator can generate. Facilitators are appointed and empowered directly by the DAO, with Aave taking the lead as the first Facilitator on the protocol.

Despite sharing a decentralized minting and burning mechanism with DAI, GHO introduces a significant departure in its operational design — shifting from vault-specific minting to position-based minting.

Vault-specific minting, as employed by DAI, ties the number of tokens in circulation to the assets deposited in the DAI vault. For every DAI minted, a corresponding value of collateral assets is locked in MakerDAO’s vault — a system known as Collateralized Debt Position (CDP).

Position-based minting, as proposed for GHO, takes a slightly different, and arguably more resource-efficient, approach. When a borrower commits an asset to the GHO smart contract, they establish a position equal to the value of their collateral within the protocol. The borrower can then mint GHO against this position, either gradually or all at once. As such, the circulating GHO supply represents the minted stablecoins, but doesn’t necessarily equate to the total value of assets held in the vault. This innovative design brings a novel dynamic to the stablecoin landscape, setting GHO apart from its peers.

The classification of crvUSD according to the ITC

The International Token Classification (ITC) is a multi-dimensional, expandable framework for the classification of tokens. In this example we will classify the crvUSD token according to the latest version of our ITC.

Economic Purpose (EEP): crvUSd is listed as a USD-Pegged Payment Token (EEP21PP01USD) due to its design.

Industry Type (EIN): The issuer of crvUSD is active in the field of Decentralized Exchanges, Markets and Market Making (EIN06DF01).

Technological Setup (TTS): crvUSD is listed as Ethereum ERC-20 Standard Token (TTS42ET01).

Legal Clam (LLC): crvUSD does not entitle its holder to any legal claim or rights against the issuing organization, therefore, it is listed as a No-Claim Token (LLC31).

Issuer Type (LIT): The dimension “Issuer Type” provides information on the nature of the issuer of the token. The Issuer Type for crvUSD is a Application Layer Protocol (LIT62AL).

Regulatory Framework (EU) (REU): The dimension “Regulatory Status EU” provides information of the potential classification of a token according to the European Commission’s proposal for a Regulation on Markets in Crypto Assets (MiCA, Regulation Proposal COM/2020/593 final). crvUSD qualifies as a Other-in-scope Crypto Asset (REU51ZZ) according to the definition provided in Article 3 (5) of Regulation Proposal COM/2020/593 final.

Consensus Mechanism (TCM): The dimension describes the mechanism that is deployed to achieve consensus on the token’s distributed ledger. crvUSD transitioned is issued on top of the Ethereum blockchain; therefore, it is listed as Proof-of-Stake (TCM71PS).

Type of Maximum Supply (EMS): The Dimension Type of Maximum Supply forms part of the Economic Dimensions Group and describes the token’s type of maximum supply. Currently crvUSD is listed as Discretionary supply token (EMS82DC).

Primary Mode of Origination (EMO): The Dimension Mode of Origination forms part of the Economic Dimensions Group and describes how the majority (>50%) of the circulating token supply got allocated to its owners. The crvUSD token is listed in the Tokenbase as Other Primary Mode (EMO96) because of its burn and mint characteristics.

Taxes (RTA): One common distinction can be drawn between crypto-assets: those crypto-assets that resemble ‘conventional’ assets, like securities, and which are merely recorded on DLT systems (Conventional Asset Tokens DTA71), and those assets and activities that raise new regulatory challenges such as virtual currencies (New Asset Tokens DTA 72; OECD 2020). crvUSD is listed in the Tokenbase as a New Asset Token (RTA72).

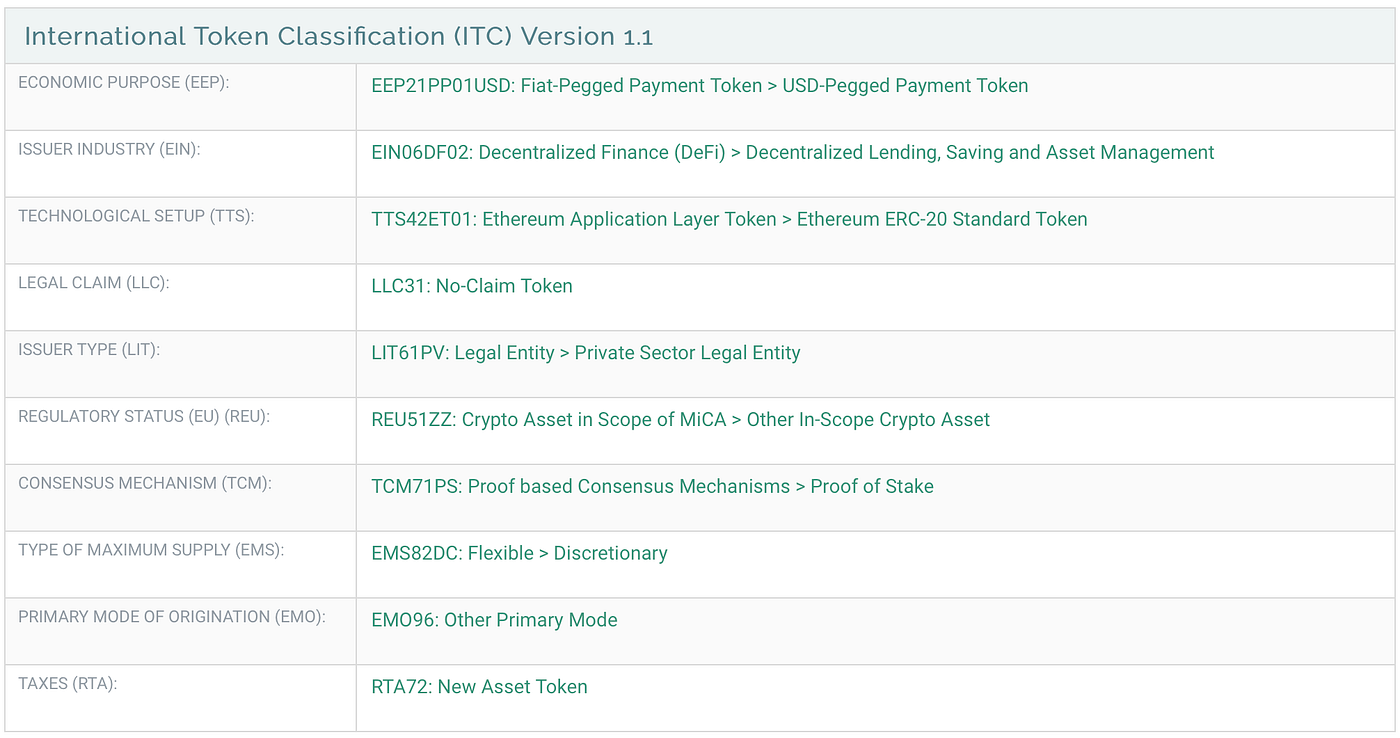

The classification of GHO according to the ITC

The International Token Classification (ITC) is a multi-dimensional, expandable framework for the classification of tokens. In this example we will classify the GHO token according to the latest version of our ITC.

Economic Purpose (EEP): GHO is listed as a USD-Pegged Payment Token (EEP21PP01USD) due to its design.

Industry Type (EIN): The issuer of GHO is active in the field of Decentralized Lending, Saving and Asset Management (EIN06DF02).

Technological Setup (TTS): GHO is listed as Ethereum ERC-20 Standard Token (TTS42ET01).

Legal Clam (LLC): GHO does not entitle its holder to any legal claim or rights against the issuing organization, therefore, it is listed as a No-Claim Token (LLC31).

Issuer Type (LIT): The dimension “Issuer Type” provides information on the nature of the issuer of the token. The Issuer Type for GHO is a Private Sector Legal Entity (LIT61PV).

Regulatory Framework (EU) (REU): The dimension “Regulatory Status EU” provides information of the potential classification of a token according to the European Commission’s proposal for a Regulation on Markets in Crypto Assets (MiCA, Regulation Proposal COM/2020/593 final). GHO qualifies as a Other-in-scope Crypto Asset (REU51ZZ) according to the definition provided in Article 3 (5) of Regulation Proposal COM/2020/593 final.

Consensus Mechanism (TCM): The dimension describes the mechanism that is deployed to achieve consensus on the token’s distributed ledger. GHO transitioned is issued on top of the Ethereum blockchain; therefore, it is listed as Proof-of-Stake (TCM71PS).

Type of Maximum Supply (EMS): The Dimension Type of Maximum Supply forms part of the Economic Dimensions Group and describes the token’s type of maximum supply. Currently GHO is listed as Discretionary supply token (EMS82DC).

Primary Mode of Origination (EMO): The Dimension Mode of Origination forms part of the Economic Dimensions Group and describes how the majority (>50%) of the circulating token supply got allocated to its owners. The GHO token is listed in the Tokenbase as Other Primary Mode (EMO96) because of its burn and mint characteristics.

Taxes (RTA): One common distinction can be drawn between crypto-assets: those crypto-assets that resemble ‘conventional’ assets, like securities, and which are merely recorded on DLT systems (Conventional Asset Tokens DTA71), and those assets and activities that raise new regulatory challenges such as virtual currencies (New Asset Tokens DTA 72; OECD 2020). GHO is listed in the Tokenbase as a New Asset Token (RTA72).

References

The International Token Standardization Association (ITSA) e.V.

The International Token Standardization Association (ITSA) e.V. is a not-for-profit association of German law that aims at promoting the development and implementation of comprehensive market standards for the identification, classification, and analysis of DLT- and blockchain-based cryptographic tokens. As an independent industry membership body, ITSA unites over 100 international associated founding members from various interest groups. In order to increase transparency and safety on global token markets, ITSA currently develops and implements the International Token Identification Number (ITIN) as a market standard for the identification of cryptographic tokens, the International Token Classification (ITC) as a standard framework for the classification of cryptographic tokens according to their inherent characteristics. ITSA then adds the identified and classified token to the world’s largest register for tokens in our Tokenbase.

- The International Token Identification Number (ITIN) is a 9-digit alphanumeric technical identifier for both fungible and non-fungible DLT-based tokens. Thanks to its underlying Uniform Token Locator (UTL), ITIN presents a unique and fork-resilient identification of tokens. The ITIN also allows for the connecting and matching of other media and data to the token, such as legal contracts or price data, and increases safety and operational transparency when handling these tokens.

- The International Token Classification (ITC) is a multi-dimensional, expandable framework for the classification of tokens. Current dimensions include technological, economic, legal, and regulatory dimensions with multiple sub-dimensions. By mid-2021, there will be at least two new dimensions added, including a tax dimension. So far, our classification framework has been applied to 99% of the token market according to the market capitalization of classified tokens.

- ITSA’s Tokenbase currently holds data on over 4000 tokens. Tokenbase is a holistic database for the analysis of tokens and combines our identification and classification data with market and blockchain data from external providers. Third-party data of several partners is already integrated, and API access is also in development.

Remarks

If you like this article, we would be happy if you forward it to your colleagues or share it on social networks. More information about the International Token Standardization Association can be found on the Internet, on Twitter, or on LinkedIn.

Valentin Kalinov is an Executive Director at International Token Standardization Association (ITSA) e.V., working to create the world’s largest token database, including a classification framework and unique token identifiers and locators. He has over five years of experience working at BlockchainHub Berlin in content creation and token analysis, as a project manager at the Research Institute for Cryptoeconomics at the Vienna University of Economics and token analyst at Token Kitchen. You can contact Valentin via valentin.kalinov@itsa.global and connect on Linkedin if you would like to further discuss ITSA e.V. or have any other open questions.

Christian Viehof is an Executive Director at the International Token Standardization Association (ITSA) e.V., working to create the world’s largest token database including a classification framework and unique token identifiers and locators. He completed his Bachelor in Economics at the University of Bonn, the Hong Kong University and the London School of Economics and Political Science with a focus on Behavioral Economics and Finance. Currently pursuing his Master of Finance at the Frankfurt School of Finance and Management, you can contact him via christian.viehof@itsa.global and connect with him on Linkedin, if you would like to further discuss ITSA e.V. or have any open questions.